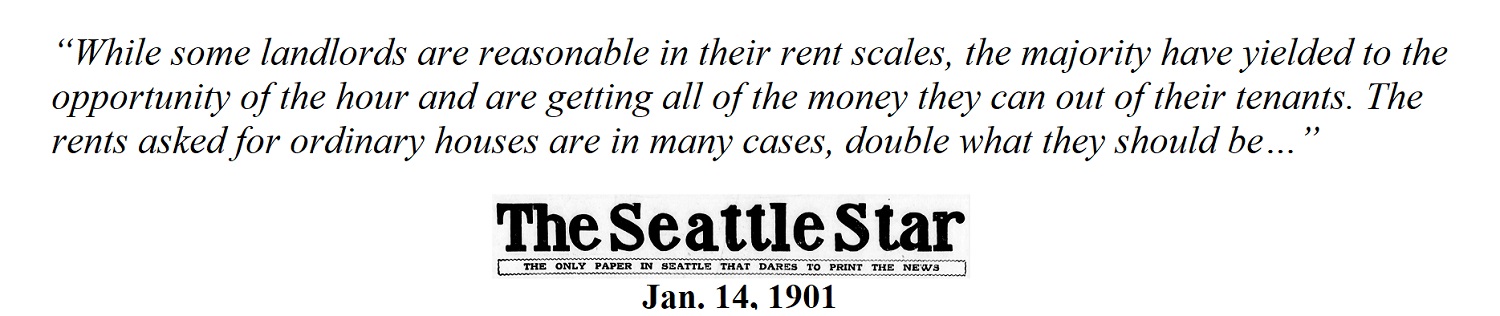

The words printed in one of Seattle’s long-gone dailies at the start of last century could arguably have been written a week ago by a member of The Seattle Times editorial board. Today, rents are also high in our fair city – and many others, from Honolulu to Hoboken – in the midst of difficult times in this nation’s history.

Across the Seattle-Bellevue-Everett area, rents are averaging $1900 a month – about the same as this time last year. But what happens after state and local governments lift their ban on rent increases?

While we don’t own a crystal ball, it’s a safe bet that landlords will take the first opportunity they get – legally, of course – to put their hand out seeking more money to cover pandemic-related costs (increased cleaning routines and sanitizing supplies, a backlog of maintenance work and new services).

And for many, that’s apparently okay. Over a 10-year period ending in 2017, Seattle experienced the highest increase in “wealthy renters” in the U.S. Defined as rental households earning more than $150,000, there are some 21,300 of this classification in our area, up from 2,900 just a decade earlier.

During the same timeframe the number of homeowners in Seattle doubled, growing to 63,400, according to a 2019 report analysis by RENT Café, a nationwide internet listing service.

There is no question: It is difficult for anyone to enter the housing market today. In addition to facing rising rents (unless living rent-free with relatives), aspiring buyers are often shouldered with great student debt loads and rising cost-of-living expenses (Have you shopped for fresh meat lately?!) that make it difficult to save.

And, yet, amid the pandemic and recession, there are still strong signals of a robust housing market and growing drive to own a home rather than continue pouring money down the drain on rent. In a June survey from Fannie Mae, 61% of Americans said now is a good time to buy a home, up from 52% in May. And 81% of all buyers viewed a home purchase as a good investment, according to a National Association of Realtors® (NAR) homebuyer profile report for 2020.

To be sure, this is not a call for everyone to leave their rental home for a single-family house in the suburbs. Many prospective buyers have lost their jobs or been furloughed and forced to draw from the savings set aside for their dream home.

If a typical millennial household had to use its down-payment savings to pay for living expenses, it would take 9 months of saving 10% of take-home pay to recoup just one month’s expenses, according to a June report from realtor.com. So, this is not a calvary charge to the next available house on the market for everyone.

In “normal” days, saving for a down payment was among the biggest obstacles to a home purchase, with 28% of buyers needing 5-plus years to make it work financially. But many people are finding a way to save for that next home – in many cases their first.

Debt is delaying younger millennials’ ability to save for a down payment by about 2 years. Student loans are delaying home purchases for 58% of millennials. About 5 million millennials are turning 30 this year.

The first-time buyer share of U.S. home sales rose from 32% in February to 35% in June, an unprecedented expansion right in the heart of the pandemic, surging unemployment and a shocking 25% of millennials planning to buy this year who acknowledge having less than $1,000 in savings.

These buyers are finding low down-payment options available today have cut the time it takes to save 5% or 3.5% by half or more, according to a new analysis from realtor.com.

Buyers in their 20s are putting down a median of 8%, an increase from 6% in 2019, but the median down payment for all buyers fell from 13% to 12% over the past year, according to the NAR’s Generational Trends Report for 2020. First-time buyers put down a median of 6%, down from 7% a year earlier but up from 4% in 2013.

Thirty-two percent of first-time buyers used help from friends or family to purchase a home in 2019, up from 29% a year earlier. Millennials are about three times more likely to get help from a family member for a down payment than older generations, and those who ask for assistance expect $10,000 from family. Many first-time buyers combine this with their own savings, as 78% of first-time buyers did use savings to purchase.

Nearly one-quarter of first-time buyers move directly from their parents, friends or family members’ home into homeownership. This share has steadily increased from a low of 12% in 1993 to 23% today.

While renting is still the most common prior living arrangement for first-time buyers, it has steadily decreased from a high of 82% to a low of 71%.

It’s important to note, that if a buyer is getting funds from a family member, the giver will have to sign a letter saying that no repayment is necessary. If the money is termed a loan, it will have to be included in the buyer’s debt-to-income ratio. If the money is coming out of a traditional 401(k) or IRA, the giver would not only owe taxes, but a large withdrawal could bump him/her into a higher tax bracket for the year.

Depending on the situation, cosigning could be a good option as well. Consulting with a loan advisor or financial planner would help provide the best course of action.

====================================

The Great Debate: Rent or Own a Home in Seattle (March 2019)

====================================

As part of their mortgage application, Amazon and other tech company employees can use their restricted stock units (known as RSUs) as part of their income, usually after two years’ employment.

Another growing segment of buyers get help through down-payment assistance programs from the state. First-time, home-buyer programs can help people with 0% interest loans but applicants generally have to work with lenders trained by the commission on the various programs.

And speaking of interest rates, the 30-year, fixed-rate mortgage averaged 3.16% at the end of June (and even lower for some people in July). The fact that mortgage rates are fixed while rents fluctuate are another reason to strongly consider the equity-building of homeownership over leasing a home.

The average interest rates for millennials were lower in May, down to 3.42% from 3.48% in April, according to the Ellie Mae Millennial Tracker. Older millennials (borrowers between 30 and 40 years old) locked in an average of 3.41% interest rate, slightly lower than 3.42% for younger millennials (aged 21 to 29 years old).

With rates down to some of their lowest levels, the share of mortgage purchases made by all millennial borrowers grew 2 percentage points to 47% in May – the first month-over-month increase since November 2019.

Buyers moving out of a rental property should strategize over the timing of the closing and move-out to avoid paying both an extra month’s rent and getting hit with prepaid interest on a new mortgage that is included in closing costs in the early part of the month. Talk to your mortgage lender about getting the timing just right.

And please speak with me when you’re ready to start buying that dream home.